New Fund Adviser Rules: Reshaping the Future of Venture Capital?

Or just some red tape and more of the same?

Over the past decade, the venture landscape has changed dramatically–from cross-over funds to syndicates and SPVs to SPACs–the industry isn’t just bigger–it's evolving. The industry boasts over 4,000 funds managing close to $100 billion in assets. Platforms like Sydecar, Carta, and Angellist have played a pivotal role in reducing the friction of operating a venture fund. The regulatory framework, however, has been without material change since the enactment of Dodd-Frank.

That has recently changed with the SEC issuing an Adopting Release of rules and amendments under the Investment Adviser’s Act of 1940. The new rules are:

designed to protect investors who directly or indirectly invest in private funds by increasing visibility into certain practices involving compensation schemes, sales practices, and conflicts of interest through disclosure; establishing requirements to address such practices that have the potential to lead to investor harm; and restricting practices that are contrary to the public interest and the protection of investors.

The rules cover registered investment advisers (RIAs) and exempt reporting advisers (ERAs). Still, because most VCs are ERAs, we will focus on the key changes impacting ERAs–the “Restricted Activities Rule” and the “Preferential Treatment Rule.”

Restricted Activities Rule

The Restricted Activities Rule addresses five activities of private fund advisers, which fall into two buckets–those that require disclosure and those that require disclosure and consent.

Disclosure

Compliance Expenses - Advisers Cannot Pass the Buck (without disclosure).

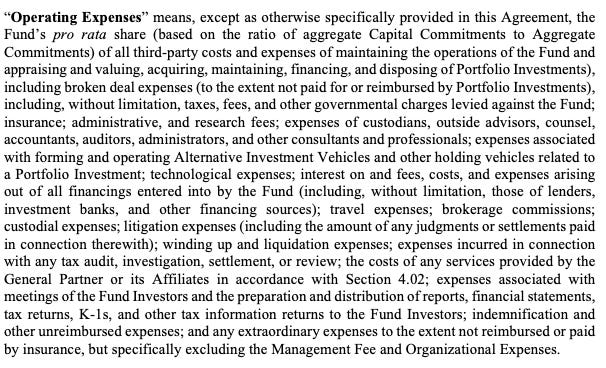

If you’ve dug into a fund’s governing documents, like an LPA, you’ve probably seen a provision stating that the fund will pay all operating expenses out of the capital commitments of the LPs. It might look something like this:

Some advisers were also charging LPs for regulatory or compliance fees and expenses like maintaining a Series 65 license or Form ADV filings.

However, with the new rules, advisers can no longer silently shift these expenses onto LPs. Instead, advisers must provide written notice within 45 days of the end of the quarter after such costs were incurred if they wish to pass these expenses onto LPs.

No Non-Pro Rata Cost Allocations (without disclosure).

An adviser may advise multiple funds invested in the same portfolio company. For instance, let’s say Junto Management Company advises three funds: (i) Junto Fund I, LP, (ii) Junto Fund II, LP, and (iii) Junto Fund III, LP, and each of those funds invested in ABC Technology, Inc., in the amounts of $1M, $3M, and $6M, respectively.

If the adviser spends $50,000 to participate in a Board meeting in Aspen (of course, skiing is involved)–how should it allocate these expenses? Common sense might say that it should be allocated among each of the funds pro rata based on the amounts invested by each fund. What if Fund I is outside of its investment period? Does that change anything?

Under the new rules, advisers cannot allocate or charge portfolio company fees and expenses among their funds on a non-pro rata basis unless the non-pro rata allocation is fair and equitable under the circumstances and the adviser delivers to the LPs a notice of non-pro rata allocation with a description of how it is fair and equitable under the circumstances before making such charges or allocations.

Again, this seems like a fairly common-sense rule and allows advisers to deal with non-pro rata situations by communicating the allocation and its reasoning to LPs.

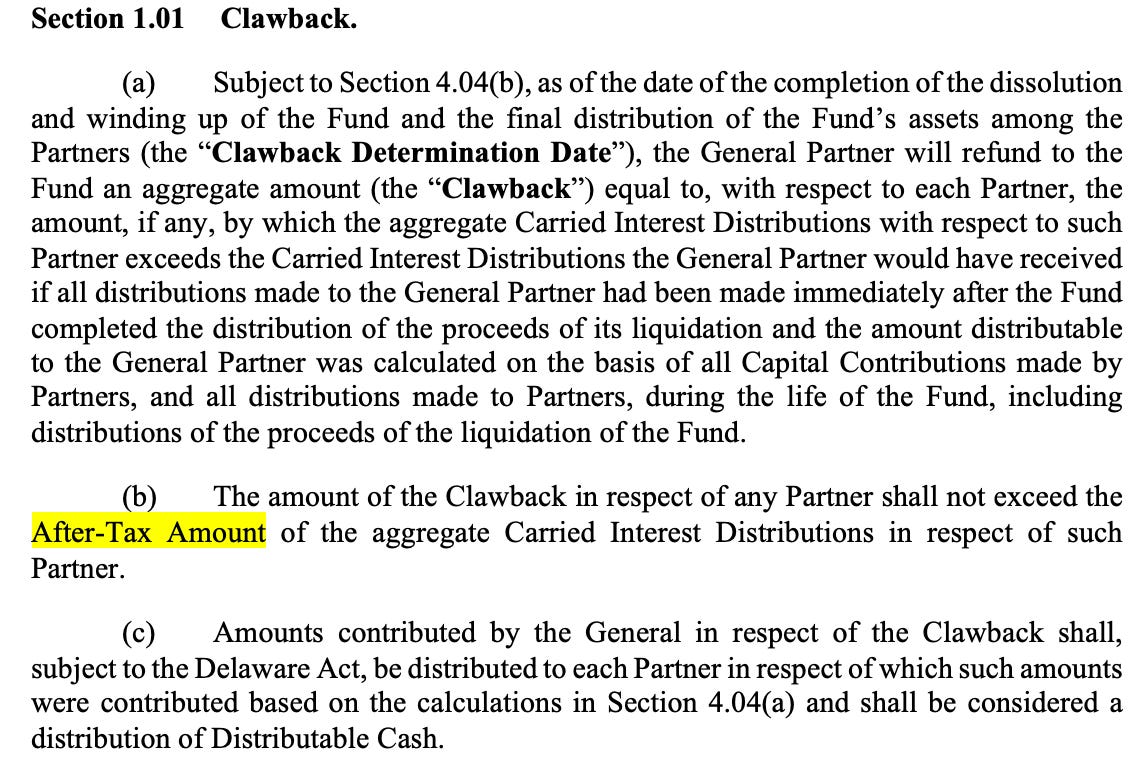

No Reduction of Clawbacks for Tax Allocations (without disclosure).

Generally, clawbacks come into play when a VC receives a distribution of its carried interest before all of the results of all fund investments coming to fruition. For instance, the GP receives a distribution related to an early investment liquidating at a profit, but once all of the investments are resolved, the GP wouldn’t have been entitled to that distribution of carry. Usually, in that situation, the LPs would be entitled to clawback all or a portion of those distributions.

VCs, however, got a bit creative and essentially argued that the full amount of the clawback should not apply because the VC had to pay taxes on those distributions, and it is not fair not to factor those tax allocations into the clawback.

Advisers must provide written notice to the LPs, including the amounts of the clawback both before and after any such tax reductions, within 45 days after the end of the quarter in which the clawback occurs if the adviser intends to adjust the amount of the clawback due to tax allocations.

Consent Required

Regulatory Investigations - No More Passing the Charge to LPs (well kinda).

If you look back at the definition of operating expenses in our example above, its broad, and some definitions of Operating Expenses might expressly include costs or expenses related to regulatory investigations. For instance, if the SEC launches an investigation on a fund manager related to violations of the Advisor’s Act–should the adviser be able to pass those expenses on to the LPs? What if the investigation is related to fraud?

Under the new rules, advisers are prohibited from charging costs and expenses related to investigations by regulators unless the adviser requests consent from all the investors in the fund and obtains the consent of a majority of the LPs (excluding the interests of the adviser and its related persons).

Borrowing from Clients.

The Restricted Activities Rule also prohibits advisers from borrowing funds or receiving an extension of credit from a fund client unless the adviser requests consent from all the fund LPs and obtains the consent of a majority of the LPs (excluding the interests of the adviser and its related persons). Again, it is relatively straightforward.

Overall, and despite widespread pushback against the initial proposed rules–the “prohibitions” of the Restricted Activities Rule are relatively straightforward, promote transparency, and provide advisers with a path for engaging in those “prohibited” activities (e.g., disclosure and/or consent).

Preferential Treatment Rule

Unlike the Restricted Activities Rule, the Preferential Treatment Rule is a bit more vague and onerous. Generally, it prohibits advisers from providing certain kinds of preferential treatment to its investors unless it satisfies certain disclosure requirements.

It’s customary for certain LPs to receive preferential treatment through side letters, which are written agreements made between a fund and an LP, granting the LP specific rights and privileges that may not be granted to other LPs (e.g., reduction in management fees, special approval rights).

The landscape for referential treatments is set to change (kind of). The SEC will still allow advisers to offer special terms to LPs, but only if the fund discloses that preferential treatment to other LPs and potential LPs.

Redemptions.

The new rules prohibit advisers from granting preferential treatment to investors concerning redemptions if the adviser reasonably expects to have a material, adverse effect on other investors unless such redemptions are required by law or offered to all investors.

This shouldn’t be a huge issue because many VCs are ERAs under Section 203(l) of the Adviser Act (e.g., a venture capital fund pursuing a venture strategy), which already includes prohibitions on redemptions.

Broad Prohibition on Preferential Treatment.

The Preferential Treatment Rule also prohibits advisers from granting any other preferential rights to investors unless the adviser delivers written disclosures specifically describing the preferential treatment provided by the adviser (or its related persons) to prospective and current investors.

Arguably, this is the most impactful change for advisers. Side letters can include a multitude of different preferential or different treatment rights. For instance, the new rules would require disclosure of preferential treatment related to information rights (e.g., GP grants an LP more detailed information rights related to a portfolio investment or fund performance) or economic rights like a reduction in management fees.

What about different rights related to an LP’s tax or regulatory status–should those be disclosed? Arguably, it could be challenging to determine whether rights are merely different or preferential.

Although the disclosure promotes transparency and is not unduly burdensome, it could tick off a lot of LPs. Many LPs negotiate specific preferences in side letters, and even if they get what they asked for, seeing another LP gain additional or different preferences may raise a few eyebrows. And what about LPs that didn’t receive any preferential rights–how happy will they be? Not to mention issues related to side letters with most favored nation provisions.

Legacy Status

Finally, the SEC will also recognize legacy status for the prohibitions provided by the rules, eliminating the need for advisers to amend governing documents entered before the effective date.

The rule will take effect 60 days following publication in the Federal Register. There are staggering compliance dates ranging from 12-18 months, depending on the rule and the size of the adviser.

Conclusion

Understanding the regulatory shifts is crucial in a rapidly evolving venture capital landscape. The SEC's new rules are more than just administrative updates; they signify an effort to bring more transparency, fairness, and accountability to an industry experiencing unprecedented growth.

While some may view them as additional red tape, others see them as necessary steps towards a more equitable and transparent future. As the industry continues to adapt and grow, it will be fascinating to see how these regulations shape the decisions of fund managers, investors, and startups alike.

If you like this post, you should follow me on Twitter, check out what we are building, or set a time to chat.

Disclaimer: While I am a lawyer who enjoys operating outside the traditional lawyer and law firm “box,” I am not your lawyer. Nothing in this post should be construed as legal advice, nor does it create an attorney-client relationship. The material published above is only intended for informational, educational, and entertainment purposes. Please seek the advice of counsel, and do not apply any of the generalized material above to your facts or circumstances without speaking to an attorney.

|

|