The Doomsday Filing: A VC's Guide to the BE-180

Or, How I Learned to Stop Worrying and Love the Bureau of Economic Analysis

"Gentlemen, you can't fight in here! This is the War Room!”

Lately, I've been on a classic movie kick, and that line from Kubrick’s Dr. Strangelove keeps rattling around in my head. It captures the absurdity of focusing on the wrong battles, especially when there is a stealth bomber directly overhead.

While we’ve been in the war room dissecting the in-and-outs of the Windsurf saga, worrying about whether the AML Rule will go into effect next year, and high on QSBS 2.0, a serious threat (dare I say a “doomsday machine”) looms. And no one is talking about it.

Seriously. This is the quiet part of the movie, right before the jump scare.

That eerie silence is the sound of the Bureau of Economic Analysis (BEA) polishing its pens, preparing to drop its own little compliance bomb on the venture world: the BE-180 Benchmark Survey of Financial Services Transactions Between U.S. Financial Services Providers and Foreign Persons.

This isn't some optional checkbox; it's a mandatory, five-year benchmark survey covering your fund's 2024 fiscal year, with a compliance deadline of July 31, 2025. That’s right, its due next week, has harsh penalties, and the BEA estimates it will take at least 11 hours to file (but from our experience, probably longer).

So, if you manage a fund with foreign LPs, it’s time to review the Big Board. This post is an overview of the filing requirements, figuring out who in your structure chart needs to file, and what you need to report.

What is Form BE-180?

The purpose of Form BE-180 is to “obtain reliable and up-to-date information on financial services transactions between U.S. financial services providers and foreign persons.”

In essence, it’s the government's attempt to map the import and export of financial services. The BEA, a branch of the Commerce Department, uses this data to build a picture of the national economy, inform trade policy, and analyze the impact of cross-border services on the U.S. balance of payments.

As the Trump administration has become focused on trade balances and tariffs, understanding the flow of services (not just goods) has become a matter of economic intelligence and security. It's not about investor protection like the SEC's rules; it’s about economic statecraft.

And they are serious about it. Filing is mandatory under the International Investment and Trade in Services Survey Act. Failure to report can lead to civil penalties, and a willful failure can bring criminal charges, including fines and imprisonment for individuals. Yes, you read that right… jail time.

“Who, Exactly, is the ‘U.S. Reporter’?”

For those of us who love a good structure chart, here is where things get fun. Form BE-180 isn’t filed by every entity in your organization, or even the entity you would most suspect (but the entity you would perhaps most medium suspect).

It’s filed on a consolidated basis by the “fully consolidated U.S. domestic enterprise." This is the top-level U.S. entity in an ownership chain that isn't more than 50% owned by another U.S. entity.

This consolidation rule is the source of major confusion. Many assume the management company files because it ultimately receives the management fee.

However, the payment from a domestic fund to a domestic management company is a domestic-to-domestic transaction (which is the structure for most funds), which is outside the scope of the Form. Instead, the purpose is to track the provision of financial services between foreign persons and U.S. persons.

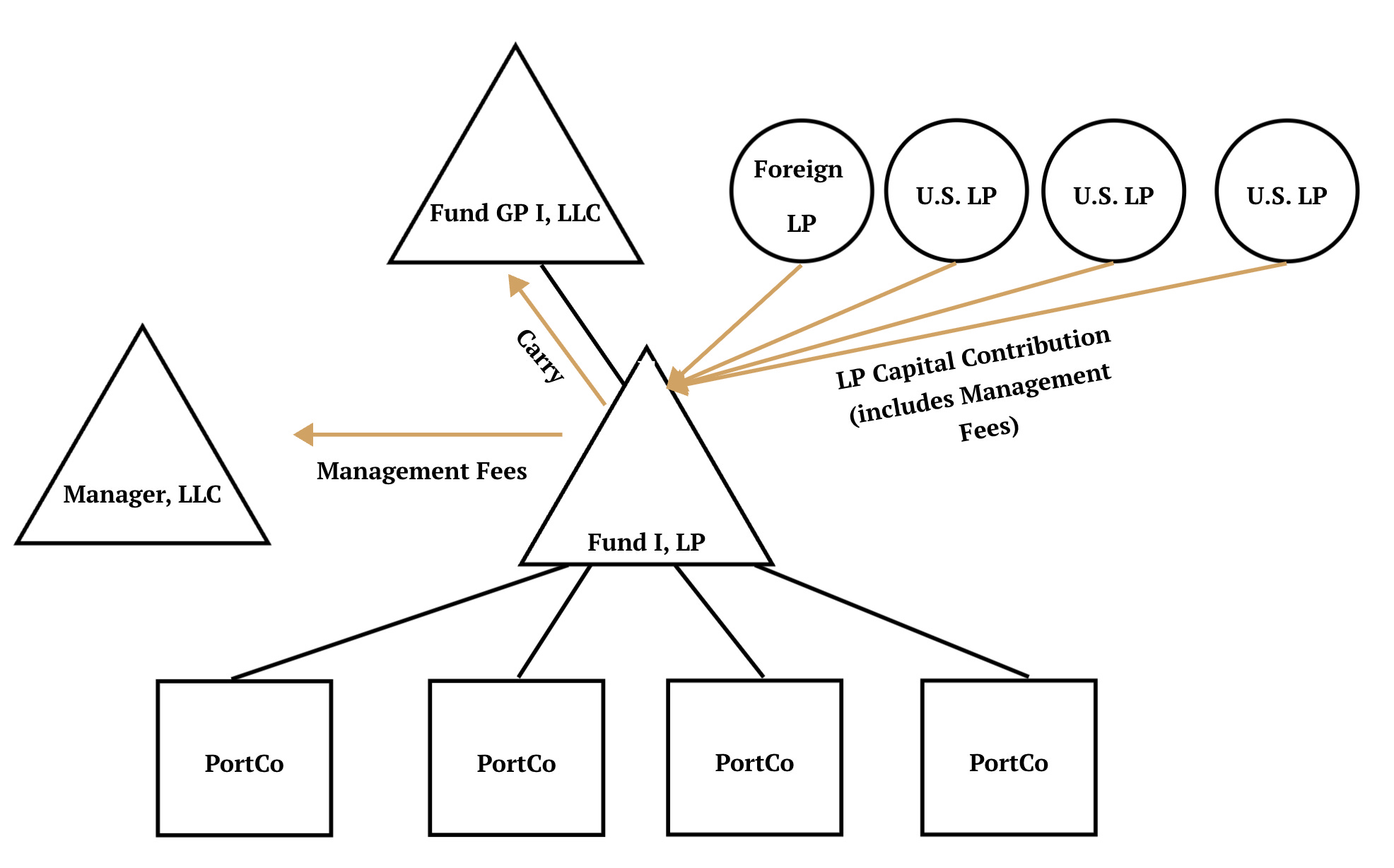

Let’s translate this using a classic fund structure:

The Setup

You have a Delaware LP (the "Fund"), a Delaware LLC as its General Partner (the "GP"), and an affiliated Delaware LLC as the Management Company (the “Manager” or “Management Company”). The Fund has several foreign Limited Partners (“LPs”).

The Consolidation Rule

The BEA’s rules state that a GP is presumed to control a limited partnership (i.e., the Fund). This means the GP and the Fund it manages are treated as a single, consolidated entity for reporting purposes.

The Answer

Because the GP controls the Fund, it becomes the U.S. Reporter. It must file a single, consolidated Form BE-180, which must account for the carried interest that are attributable to the capital invested by foreign LPs, even though the cash flows through the Fund first.

However, according to BEA guidance, management fees for U.S. funds (like mutual funds, hedge funds, or trusts) are generally not reportable unless charged directly to a foreign investor, rather than to the U.S. fund itself. "Direct charge" typically means a separate invoice, wire, or obligation from the investor to the provider (e.g., adviser), not a pooled fund payment. Whether this applies depends on the specific structure of your fund and its governing documents (e.g., if fees are framed as direct obligations of foreign LPs in subscription agreements, they may be reportable; otherwise, they might be treated as domestic transactions.

The payment from the Fund to the Management Company is disregarded, unless of course the Management Company also controls the GP (e.g., owns 51% of the voting securities or is the manager of the manager-managed LLC).

For example, on a $100M fund with a 2% management fee and 40% of its capital coming from foreign LPs, the reportable management fee is $800k (2% of the $40M in foreign capital), which would need to be included on the Form (assuming that was the amount for 2024) if structured as a direct charge.

The Counterintuitive Twist: Your Carried Interest is a “Service Fee”

According to BEA guidance, profit allocations are reportable as financial management fees because they are considered compensation due to fund performance. This means carried interest is considered a payment for financial management services and is reportable. This applies to carried interest received by a domestic GP from both foreign funds and domestic funds with foreign investors.

This requires you to:

Calculate the Carried Interest Attributable to Foreign LPs: You need to determine the portion of your accrued carry for fiscal year 2024 that is economically tied to the capital from your foreign investors.

Report it as a "Sale": This amount, along with management fees from foreign LPs, gets reported as a "sale" of "financial management services" (subject to the nuances above).

To put numbers on it: Imagine that same $100M fund returns $200M. After returning the $100M of capital, there's $100M in profit. With a standard 80/20 split, the GP's carried interest is $20M. Since 40% of the fund's capital came from foreign LPs, the reportable amount of carry for the BE-180 is $8M (40% of $20M).

The Nitty-Gritty: Thresholds, Deadlines, and How to Comply

The BE-180 has reporting thresholds, but they’re not as straightforward as you’d hope.

Full Reporting ($3M+): If your consolidated enterprise had combined sales of covered services to foreign persons exceeding $3 million OR combined purchases from foreign persons exceeding $3 million in fiscal year 2024, you must complete the entire, detailed survey. Note that these thresholds are separate; hitting one is enough to trigger the full filing.

Partial Reporting (<$3M): If you had any reportable transactions but your total sales and purchases were each $3 million or less, you still have to file, but only a truncated version of the form (through Question 7). There is no de minimis exemption; a single dollar of reportable fees from a foreign LP technically requires a filing.

Exemption Claim: If you were contacted by the BEA but have zero reportable transactions, you must file an exemption claim by completing the determination section of the form. Ignoring the notice is not an option.

The deadline for all of this is July 31, 2025. If you need more time, you can request an extension in writing before the deadline. The BEA provides a specific email for this: be-180extension@bea.gov.

Key Takeaways and Your Compliance Game Plan

Where everyone was talking about the Beneficial Ownership Information Reports and the AML Rule (which has been pushed back until 2028), the BE-180 survey is the stealth bomber of a compliance requirements. Here’s your game plan:

Acknowledge the Obligation is Real: If you have foreign LPs, you need to do the analysis. This isn't optional. Your status as an Exempt Reporting Adviser doesn't get you a pass.

Identify Your U.S. Reporter: Pull out the structure chart and apply the BEA’s consolidation rules. The controlling GP of a domestic fund is likely the filer, not necessarily the management company that gets the fee. However, it depends on your documents and structure.

Embrace the Weirdness of "Service Fees": Accept that for the purpose of this form, your carried interest is a reportable service fee. Begin the process of calculating the accrued value attributable to your foreign LPs for fiscal year 2024 now. This will probably not be a simple data pull.

Assess Your Thresholds: Aggregate your foreign management fees and carry to see if you cross the $3 million threshold for a full filing.

File Something: Whether it’s a full report, a partial report, an exemption claim, or a request for an extension, you likely need to submit something to the BEA by July 31, 2025.

Hey, I am Shayn. I am the Founder of Junto Law. If you like this post, follow me on X or set a time to chat.

Disclaimer: While I am a lawyer who enjoys operating outside the traditional lawyer and law firm “box,” I am not your lawyer. Nothing in this post should be construed as legal advice, nor does it create an attorney-client relationship. The material published above is only intended for informational, educational, and entertainment purposes. Please seek the advice of counsel, and do not apply any of the generalized material above to your facts or circumstances without speaking to an attorney.